1. Overpaying for auto insurance (by up to $461/year)

Believe it or not, the average American family still overspends by $461/year¹ on car insurance.

Sometimes it’s even worse: I switched carriers last year and saved literally $1,300/year.

Here’s how to quickly see how much you’re being overcharged (takes maybe a couple of minutes):

- Pull up StopOverpaying.org – it’s a free site that will compare offers for you

- Answer the questions on the page

- It’ll spit out a bunch of insurance options

That’s literally it. You’ll likely save yourself a bunch of money.

Here’s a link to StopOverpaying.org

2. Paying off credit card debt on your own

If you’ve got $10k+ in unsecured debt (think credit cards, medical bills, etc), you could use a debt relief program and potentially reduce it by around 23% (on average).

Here’s how to quickly see if you qualify for debt relief:

- Head to the National Debt Relief's site here

- Answer the questions on the page

- Find out if you qualify

- Simple as that. You'll likely end up paying less than you owed and could be debt free in 24-48 months.

Here’s a link to National Debt Relief.

3. Getting price-gouged when you shop online

You might be surprised how often you’re overpaying on Amazon and elsewhere.

Big stores like Amazon know that no one has time to price shop through dozens of sites, so there’s often no incentive for them to offer bargain prices.

I typically hate browser extensions with a fiery passion, but if you don’t have Capital One Shopping installed yet, do yourself a favor and grab it.

When you shop online (on Amazon or elsewhere) it will:

- Auto-apply coupon codes to potentially help save you money

- Compare prices from other sellers to help make sure you’re not missing out on a better deal

Here’s a quick example of how it works:

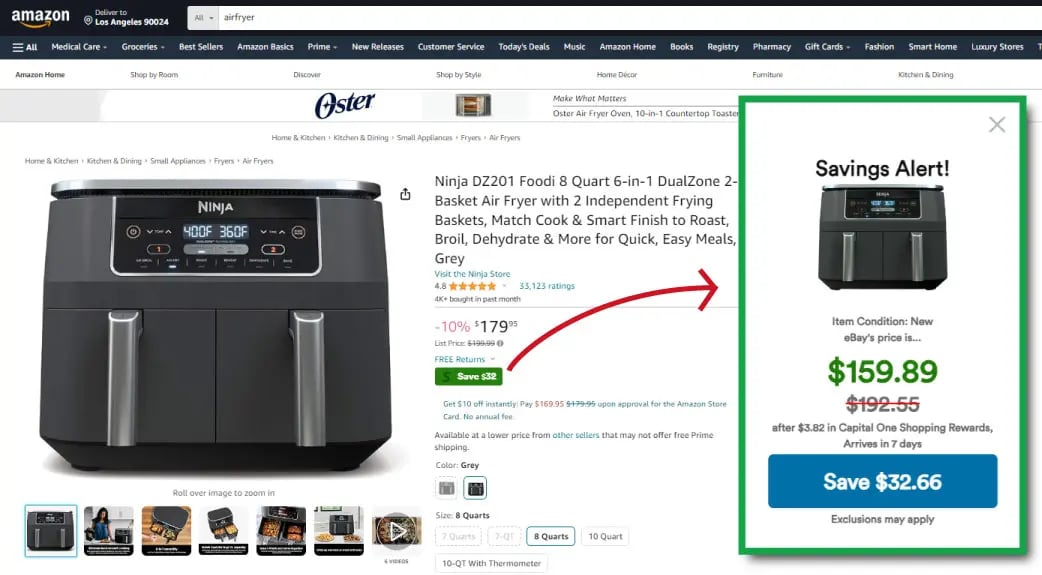

Savings will vary, this is just an example, of course.

Whenever the extension finds an available discount, you’ll see a little savings alert pop-up. For example, here you can save $32 on this air fryer.

Here’s a link to install Capital One Shopping, if you’re interested.

4. Ignoring your home equity

If you own your home but are low on funds, you might want to look into a HELOC (home equity line of credit). Instead of borrowing from your bank, you can essentially borrow from yourself (by tapping into your home's equity).

They may have lower interest rates and more flexible terms that a typical loan would.

Here’s a free page you can use to see how much you could access: link.

5. Not having a financial advisor

Most people don’t have one, and it’s typically a huge mistake.

Sure, you can manage things on your own if you want to, but most people don’t have the time to actually do things right. There are huge benefits to having somebody pay attention to your money all the time.

People with financial advisors tend to beat the market by ~3%/year

(according to a 2019 Vanguard Study). That can make a huge difference over time.But more important: a good advisor will handle ALL of the annoying retirement stuff & bizarro tax implications you would have never thought of.

If you don’t know a financial advisor personally, use a comparison site (like Datalign) and find somebody near you that has good reviews.

Or if you want something easier, here’s a quiz you can fill out that can find an advisor/planner based on your reqs.

6. Not blocking ads on your computer or phone

If you aren’t using an ad blocker yet, I am begging you to try one. I am not exaggerating when I say it will change your life.

A good ad blocker will eliminate virtually all of the ads you’d see on the internet.

No more YouTube ads, no more banner ads, no more pop-up ads, etc. It’s incredible.

Most people I know use Total Adblock (link here) – it’s $2.42/month, but there are plenty of solid options.

Ads also typically take a while to load, so using an ad blocker reduces loading times (typically by 50% or more). They also block ad tracking pixels to protect your privacy, which is nice.

Here’s a link to Total Adblock, if you’re interested.

7. Overpaying on home insurance.

Switching home insurance will often save you more than switching auto policies (I’ve heard of people saving $1k per year by switching).

Here’s the home insurance comparison site I typically use: link.

8. Paying way too much in credit card interest

High-interest credit card payments can be a nightmare. Have you ever wished you could just take a break from them?

You actually might be able to. Many people may not know, but there’s a great way to avoid interest payments for over a year or more.

It’s called a balance transfer. In simple terms, you move your balance to a new credit card that offers a 0% intro APR for a set period of time, which could help you save on interest.

If you’re interested, here are a few great balance transfer cards to look into: link here.

9. Paying for subscriptions you don’t even use

We’ve all signed up for free trials and forgotten to cancel them. Stop paying for services you aren’t using!

Take a minute and get yourself a good cancellation app: I like Rocket Money (link here).

It’s an app that will put together a list of your subscriptions so you can pick/choose which ones to cancel.

They also have a premium service that will cancel them for you, if you’d like.

Here’s a link (it’s free).

10. Paying more to your credit card company than you have to

If you’re stuck with credit card debt, you feel it. The high interest, the endless payments, the sinking feeling that you’re never getting ahead.

And let’s be honest—your credit card company isn’t on your side. It’s making a fortune off you with interest rates that can hit 36%.

So how do you get out of it? If you owe less than $100k, you can likely pay it off in one fell swoop using a debt consolidation loan.

Here’s how it works:

- Use a site like AmOne to look at consolidation options (many loans offer far, far lower interest rates than your credit card company does)

- Pick one that works for you

- Use that loan to pay off your credit cards

- Then, slowly pay off the debt consolidation loan over time

The upside: you’ll have just one monthly payment. And because personal loans typically come with lower rates (AmOne lenders offer options as low as 6.40% APR), you’ll get out of debt sooner. Plus, no credit card bill this month.

It takes less than 2 minutes to compare your options. No Social Security number required, just a real phone number (but don’t worry—they won’t spam you), and it won’t affect your credit score.

Here’s a link to AmOne’s site.

11. You keep paying sky-high credit card interest until at least 2027

Stop bogging yourself down with those high-interest credit card payments. It seriously limits your spending power.

If your monthly interest payments are starting to creep out of control, you might need to take a look at changing things up with your current credit card by finding a card with a 0% intro APR.

Some balance transfer cards stand out if you’re trying to take back control. These cards offer 0% intro APR on purchases and balance transfers until 2027, which means you could get the breathing room you need to tackle your debt or make a new purchase without being hamstrung by high interest for over the whole year.

On top of that, you can earn up to 5% cash back on everyday purchases with these cards and enjoy a $0 annual fee. It’s really a no-brainer when you consider you could save on interest and earn rewards on everyday purchases.

Get rid of your high-interest payments. Learn more about these cards today.